UNDERSTANDING THE

GREAT WALL STREET FRAUD (summarized)

*(12-30-07) The best

and easiest to understand analogy, though not perfect, to the wall street

markets is the kiting of checks at lightning computerized trading speed on

which commissions are taken although there is nothing of real value underlying

their fraudulent scheme.

*(12-31-07) The ubiquitous computerization of wall street functions, the

enhancement/advance/integration of the said computer equipment/peripherals in

terms of computing power and speed, along with the concomitant advance/sophistication

of the programming concerning same has enhanced the ability of the frauds on

wall street to effect their frauds with blinding speed vis-à-vis the funds

entrusted to their care by way of programmed trades, ie., buy, sell, stop

limits, etc.. An example (though not perfect) is illustrative: Dow drops 200 points as programmed sell

orders kick in with some not so fudged negative news. Nothing changes but the

following day the market rises 205 points on programmed buy orders (a little

higher despite the absence of any positive news). Hence, the huge swings which

have become ever so more prevalent. Though nothing has changed, hundreds of

millions of dollars without relation to any value added (in economic terms,

service, etc.) is taken in commissions (percentages, points, spreads) by the

frauds on wall street on huge computerized trading volume (hence, the

multi-billion dollar bonuses on top of huge salaries, etc.). The fact is that

these funds entrusted to them are so large that such computerized “buys” can

simulate other than rational demand causing prices to rise solely to generate

huge commissions to them and new funds coming in (as in a ponzi scheme). The

corrupt government has been complicit in terms of false economic reports,

legislation protecting the fraud (ie., exemption from RICO accountability,

etc.), while the courts are also corrupt facilitators (ie., new york, new

jersey, california, etc., and similarly don’t count on arbitration

panels). There was a time when

transaction costs mattered in financial investment decisions. The

trades/commissions are not a net positive for the economy but are indeed of

great benefit to the recipients of same (who like termites eat away at other

peoples’ money, and whose marginal propensity to consume is less than those

allocating their monies/pensions/401ks/savings etc.; hence, the mess to

follow). Finally, the NASDAQ/tech has become the “safe haven” but in reality as

in the dot.com bust days are just the great story without much fundamental

understanding that keeps the fraudulent ball rolling.

(1-01-08) Remember: more

contrived wasteful commissions to the wall street frauds, the level and

percentage of which should be examined in light of computerization and

decreased costs attendant to same especially since only A Very Small Fraction

Of What wall street Does Is A Net Positive For The Economy (New Investment

Capital via, ie., ipo’S), The Rest Is Tantamount To A (Economically)

"Wasteful Tax" (On The Economy) via 'churn and earn' computerized

programmed trades.

*(1-3-08)

$14 billion ($21 billion in 2006) in bonuses to the lunatic/frauds on wall

street for a commissionable (sub prime bundled) fraud well done, inflation up,

dollar down, oil prices up, manufacturing down; one analyst/reporter/journalist

from inside sources pegs the sub-prime dollar value of the shilled worthless

paper at $516 TRILLION (even a percentage of same renders the problem

unfixable-hence, culpable parties must be held accountable and disgorge their

ill-gotten gains from, ie., commissioning worthless paper, taking a point here

or there and fraudulently passing same on, ad infinitum, etc.). Of course there

are also a plethora of garden-variety frauds as always, ie., 10-B-5, insider

trading, etc..

*(10-10-08) Now to bring the initial check-kiting analogy

closer to the current crisis, realize as is the case of the worthless sub-prime

securities, there is no charge-off/debit as is ordinarily the case with a

cleared check and the worthless 'collateralized sub-prime security' is

repackaged, resold, recommissioned based upon (collateralized by) as collateral

the original worthless security which is in turn repackaged, resold,

recommissioned based upon as collateral the subsequent worthless security, and

so on (a geometric progression) to the

tune of (hundreds of) trillions of this worthless, fraudulent paper (blatent/flagrant

securities fraud which must be

prosecuted and fraudulently derived profits disgorged).

THE BAILOUT FRAUD/SCAM

This

is not brain surgery and the fraud, bonuses/compensation (mortgages, subprime

and otherwise, are only a relatively small portion of the fraud/scam providing

“cover/collateral” for the worthless but heavily commissioned paper over and

over again in a multiplicity of different forms of worthless paper) in the

mega-billions should first be disgorged before taxpayers are forced to pony up

and pay the frauds again for their fraud which caused the problem in the first

instance, must be prosecuted. It should also be noted that despite the

rhetoric, the wall street bailout will NOT solve the crisis or eliminate the

economic pain except to make permanent the fraudulent wealth transfer to the

most well healed heals/frauds/criminals in the nation who caused the so-called

crisis by their greed/corruption/fraud.

Some Economic Background to the

Current Crisis

CITIGROUP and MERRILL face

bigger writeoffs/dividend cuts, etc.....

CHEER: Ambrose

Evans-Pritchard: Bank Crisis may make '29 look 'walk in park'... As central banks continue to splash their

cash over the system, so far to little effect, Ambrose Evans-Pritchard argues

things are rapidly spiralling out of their control Twenty billion dollars here,

$20bn there, and a lush half-trillion from the European Central Bank at

give-away rates for Christmas. Buckets of liquidity are being splashed over the

North Atlantic banking system, so far with meagre or fleeting effects.

"Liquidity doesn't do anything in this situation," says Anna

Schwartz, the doyenne of US monetarism and life-time student (with Milton

Friedman) of the Great Depression."It cannot deal with ….. that lots of

firms are going bankrupt. The banks and the hedge funds have not fully

acknowledged who is in trouble. That is the critical issue," she adds…..

The

time-lines below highlight the four recessions in the US economy since

1980…..While the NBER was only a little late in its recognition of the

recession that began in Summer 1981, they were late to the game in the

remaining three. In fact, during the last two recessions, the NBER did not

officially declare the start to a recession until the recession had already

ended. The u.s. is already in recession, beyond the fake data/reports, with

much higher than reported inflation, etc..

Economic Expert

Says Global Crash Imminent

Echoes former world bank leader with prediction of global

recession Steve Watson

A leading economic expert has warned that a global crash and

recession is imminent on the back of record highs in real estate, stocks and energy,

combined with a devaluation of the dollar and continued speculative bubble

thinking. Robert Shiller, the Stanley B. Resor Professor of Economics at Yale

University told an audience at the annual Dubai International

Financial Centre (DIFC) Week that a sharp downward correction is due in the

global markets. Shiller stated: Perhaps we have gotten a little too confident

in the global economic growth, said Shiller. The problem is high oil, stock and

real estate prices. I believe that a substantial part is speculative bubble

thinking. We have gotten too confident of the prices in these markets.

Economic Outlook 2008: Darkening Clouds

Dom Armentano Lew

Rockwell.com Thursday December 6, 2007 Presidential election years usually

are not recessionary but next year will be an exception. Several economic

factors are colliding in an almost perfect storm to markedly slow the general

economy and the stock market. The most important signal flashing recession is,

of course, the sub-prime mortgage fiasco. After years of monetary inflation on

the part of the Federal Reserve, individuals and families with poor credit were

suckered into low-down-payment/low-interest adjustable mortgages that simply

cannot be maintained or repaid under current conditions. Their incentive is to

sell the property quickly before their equity evaporates and/or the financial

institution repossesses it. Yet the massive oversupply of homes and condos for

sale has pushed prices down at a record clip and made additional foreclosures

even more likely. Next year, unfortunately, will be the Year of the Auction.

The financial institutions have also been punished…well sort of. Various

institutions including hedge funds that hold these poorly performing debt

obligations have been forced (by accounting rules) to "write down"

the value of these assets, take huge paper losses in the bargain, and pull in

their financial horns. Thus, any near-term recovery in housing must now fight a

record supply availability, falling prices, higher insurance costs and

restricted credit…a near-term impossibility in my view. Moreover, the slowdown

in residential and commercial construction will send secondary ripple effects

throughout the economy. Laid-off construction workers don't spend money.

Construction and home furnishing suppliers sell less output and make fewer

investments. Even local governments will be pinched by declining property-tax

assessments and fewer developer fees. Things are likely to get worse before

they get any better. The second major factor indicating a near-term recession

is the sky-high price of crude oil and refined product. Pushed upward by

world-wide speculative Mid-East war fears and increases in demand (especially

from China), increasing energy prices act as an inflationary "tax" on

domestic production and consumption throughout the market economy. Higher costs

of production will lower profits; higher prices will reduce some consumption.

The only good news here is that any substantial economic slowdown in 2008 will

eventually moderate the price of oil and other commodity prices as well. The

third factor in the current recession scenario – and the real wild card – is

the continuing decline in the value of the dollar in international money

markets caused by our Iraq blunder and the Federal Reserve–generated oversupply

of dollars. Some economists would argue that a devalued dollar is good for U.S.

exports, and thus positive for the economy as a whole. I disagree for three

reasons. First, the bulk of crude oil purchases takes place in dollars; a

falling dollar translates into still higher crude oil prices. Second, the U. S.

dollar is the major reserve currency of the international monetary system and

dollar-paying investments (such as U.S. Treasury bills and bonds) are held in

massive amounts by foreign banks and governments. Dollar devaluation makes

these investments less attractive and any disinvestment in these areas would

sharply drive bond prices down and increase interest rates. The third reason

why dollar devaluation makes recession more likely is that it effectively

prevents the Federal Reserve from pushing U.S. interest rates much lower. Any

additional Fed easing (inflation) would be seen as a signal of even further

future dollar devaluation and even higher dollar prices for oil. Unfortunately,

we will not be able to "inflate" our way out of this recession this

time. We will simply have to take our lumps and let market forces liquidate the

bulk of the malinvestments caused by the unprecedented Greenspan money bubble.

This liquidation process will not be pretty but it is necessary to restore a

sustainable economic recovery in the years ahead.

Don’t forget: Criminal america has the

highest crime rates in the world. No other so-called ‘civilized’ nation even

comes close.

Euro gains on dollar

in official reserves...

FROM THE SUB-PRIME

TO THE RIDICULOUS: HOW $100B VANISHED...

PAPER: TOP

ECONOMIST SAYS AMERICA WILL PLUNGE INTO RECESSION...

TOP TRENDS 2008: PANIC AND FEAR http://www.trendsresearch.com

Economic 9/11

Just as the Twin Towers collapsed from the top down, so too will the

US economy from an Economic 9/11. When the high-stake speculators, banks,

brokerages, and buyout firms that leveraged billions with millions get hit ...

everything underneath them will turn to rubble.

The Panic of 08

Failing banks, busted brokerages, toppled corporate giants, bankrupt

cities, states in default, foreign creditors cashing out of US securities …

whatever the spark, the stage is set for panic in the streets. When the giant

firms fall, they'll crush the man on the street. ....

Conservation Engineers

More powerful than high tech and paying much better than the booming

health care sector, we forecast that "Conservation Engineers" and

"Conservation Specialists" that are skilled in providing enviro-smart

solutions will be among the most handsomely rewarded and sought after professions

for the next several decades.

Tax Revolts

It was a reason given for starting the first American Revolution and

as the trends add up, it will also be a reason for starting the second. Fed up,

and not willing – or able – to take it anymore, overtaxed Americans will begin

the battle against politicians and bureaucrats in the fight to lower and/or

repeal taxes… while demanding higher tax rates for those seen as paying too

little. .....

Bye, Bye Bucks

America’s going broke and the whole world knows it. Betting that its

economy will spiral down and that the dollar will fall with it, foreign

cdarkreditors are dumping dollars on the market … and even Third World street

vendors don’t want to take greenbacks any longer. The further it falls, the

less it’s worth. The less it’s worth, the less it buys. In the real world they

call it "inflation." In America they call it "good for

business." ......

Small is Big

Unlike the years of personal prosperity and business growth long

perceived a birthright … today, as America’s fortunes dwindle, its people will

be forced to adjust attitudes and alter practices to compensate for the losses.

Although the oncoming national downsizing trend may be a blow to egos and

painful to pocketbooks, if intelligently deployed and spiritually practiced,

the "Small is Big" trend can lead to more progressive advancement and

greater rewards than the supersizing trend that has been consuming much of the

nation.

Heal Yourself Health Care

Just as it took mountains of facts and bottom line realities to

finally convince a consumption prone public that energy saving tools and

environmentally sound practices bring bigger rewards and higher quality, the

oncoming "Heal Yourself Health Care" trend will be as widely embraced

and will prove equally rewarding. Evolving over the past two decades, along

with growing acceptance of seeking alternative medical options, the "Heal

Yourself Health Care" trend is being driven by both the lack of money and

the power of the mind.

TechnoSlaves.com

It’s a quickly spreading worldwide epidemic that will get much

worse. All colors, classes, creeds and races are addicted and they can’t break

the habit. Before 2008 ends, the TechnoSlave trend will be so pervasive and so

deeply embedded into the fabric of society that Old World communication styles

will be seen as quaint and ridiculed as stupidly boring by the high-tech

"hip." Across borders and around the world, blinking lights of blue

and red flash from human ears … electro-plastic appendages affixed to the body

and controlling the mind. So self-important have society’s members become that

they must be connected at all times … to be in touch and instant messaged … for

work, play and to fill the voids of idle time.

Hold on to Your Hats

2008 is going to be a wild ride. http://www.trendsresearch.com

Jeremy Grantham: All the World's a Bubble

By Brett

Arends

…..Grantham says we are now seeing the first worldwide bubble in history

covering all asset classes.

Everything is in bubble territory, he

says. Everything.

'The bursting

of this bubble will be across all countries and all assets.' -- Jeremy Grantham

|

The United States is heading for bankruptcy, according to

an extraordinary paper published by one of the key members of the country's

central bank. |

A ballooning budget deficit and a pensions and welfare timebomb

could send the economic superpower into insolvency, according to research by

Professor Laurence Kotlikoff for the Federal Reserve Bank of St Louis, a

leading constituent of the US Federal Reserve.

Prof Kotlikoff said that, by some measures, the US is

already bankrupt. "To paraphrase the Oxford English Dictionary, is the

United States at the end of its resources, exhausted, stripped bare, destitute,

bereft, wanting in property, or wrecked in consequence of failure to pay its

creditors," he asked.

According to his central analysis, "the US government

is, indeed, bankrupt, insofar as it will be unable to pay its creditors, who,

in this context, are current and future generations to whom it has explicitly

or implicitly promised future net payments of various kinds''.

Prof Kotlikoff, who teaches at Boston University, says:

"The proper way to consider a country's solvency is to examine the

lifetime fiscal burdens facing current and future generations. If these burdens

exceed the resources of those generations, get close to doing so, or simply get

so high as to preclude their full collection, the country's policy will be

unsustainable and can constitute or lead to national bankruptcy.

"..... there are strong reasons to believe the United

States may be going broke."

Experts have calculated that the country's long-term

"fiscal gap" between all future government spending and all future

receipts will widen immensely as the Baby Boomer generation retires, and as the

amount the state will have to spend on healthcare and pensions soars. The total

fiscal gap could be an almost incomprehensible $65.9 trillion, according to a

study by Professors Gokhale and Smetters.

The figure is massive because President George W Bush has

made major tax cuts in recent years, and because the bill for Medicare, which

provides health insurance for the elderly, and Medicaid, which does likewise

for the poor, will increase greatly due to demographics.

Prof Kotlikoff said: "This figure is more than five

times US GDP and almost twice the size of national wealth. One way to wrap

one's head around $65.9trillion is to ask what fiscal adjustments are needed to

eliminate this red hole. The answers are terrifying. One solution is an

immediate and permanent doubling of personal and corporate income taxes.

Another is an immediate and permanent two-thirds cut in Social Security and

Medicare benefits. A third alternative, were it feasible, would be to

immediately and permanently cut all federal discretionary spending by 143pc."

The scenario has serious implications for the dollar. If

investors lose confidence in the US's future, and suspect the country may at

some point allow inflation to erode away its debts, they may reduce their

holdings of US Treasury bonds.

Prof Kotlikoff said: "The United States has

experienced high rates of inflation in the past and appears to be running the

same type of fiscal policies that engendered hyperinflations in 20 countries

over the past century."

UPDATE - Two former NYSE

traders found guilty of fraud

Stock market staggers, but investors still may be too optimistic

Commentary: Newsletters react to stock markets' losing week

By Peter Brimelow,

MarketWatch 12:04 AM ET Jul 17, 2006

Investors may still be too optimistic

NEW YORK (MarketWatch) -- First, a proprietary word: on Friday night, the

Hulbert Stock Newsletter Sentiment Index (HSNSI), which reflects the average

recommended stock market exposure among a subset of short-term market timing

newsletters tracked by the Hulbert Financial Digest, stood at plus-23.8%. This

was certainly below the 31.4% it showed on Tuesday night, when Mark Hulbert

worried, presciently we must say, that it was too strong from a contrary

opinion point of view. But it's still above its 12.6% reading at end of June,

although, Mark pointed out, the stock market had declined in the interim. And

since Mark wrote, the Dow Jones Industrial Average has had three triple-digit

down days.

Not good.

Dow Theory Letters' Richard Russell wrote Friday morning: "If

the Dow breaks support at 10,760, I think we could have some nasty action, even

some crash-type action." But, perhaps significantly, Russell did not quite

hit the panic button when the Dow did indeed close at 10,739 Friday night.

He

simply remarked, supporting the contrary opinion view: "Three days in a

row with the Dow down over 100 points each day -- you don't see that very

often. But still no signs of real fear, no capitulation, no panic -- just down,

down, and down. The key consideration here is that there is still no sign of

big money coming into this market. In fact, the big money has been leaving this

market all year. ... The longer the market continues down without a panic decline,

the worse the ultimate panic will be when it arrives."

What is Wrong with the Stock

Market?

Dr. Khaled Batarfi

John D. Rockefeller was once asked

why he decided to sell all his stocks just months before the 1929 Wall Street

Crash. He explained: One morning, I was on the way to my office and stopped to

have my shoes polished. The guy asked my advice about the shares he bought. If

people with this kind of talent were now playing the market, I knew there was

something wrong.....

U.S. Treasury balances at Fed fell on July

17Tue Jul 18, 2006

WASHINGTON, July 18 (Reuters) - U.S.

Treasury balances at the Federal Reserve, based on the Treasury Department's

latest budget statement (billions of dollars, except where noted):

July 17 July 14 (respectively)

Fed acct 4.087 4.935

Tax/loan note acct

10.502 10.155

Cash balance 14.589

15.192

National debt,

subject to limit

8,311.633 8,323.084

The statutory debt limit

is $8.965 trillion.

The Treasury said there were $192 million in individual tax refunds

and $23 million in corporate tax refunds issued.

End Of The Bubble Bailouts

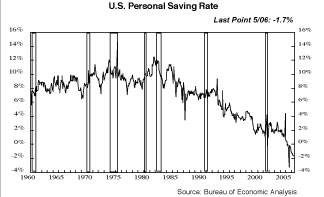

A. Gary Shilling, Insight 08.29.06 - For a quarter-century, Americans’ spending binge has been fueled by a

declining savings rate and increased borrowing. The savings rate of American

consumers has fallen from 12% in the early 1980s to -1.7% today (see chart

below). This means that, on average, consumer spending has risen about a half

percentage point more than disposable, or after-tax, income per year for a

quarter-century.

The fact that Americans are saving less and less of their after-tax

income is only half the profligate consumer story. If someone borrows to buy a

car, his savings rate declines because his outlays go up but his disposable

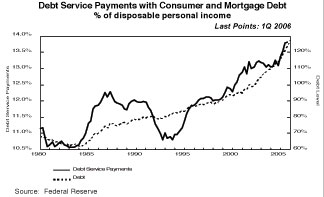

income doesn’t. So the downward march in the personal savings rate is closely

linked to the upward march in total consumer debt (mortgage, credit card, auto,

etc.) in relation to disposable income (see chart below).

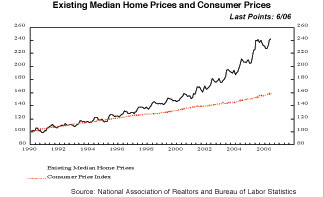

Robust consumer spending was fueled first by the soaring stock market of

the 1990s and, more recently, by the housing bubble, as house prices departed

from their normal close link to the Consumer Price Index (see chart below) and

subsequently racked up huge appreciation for homeowners, who continued to save

less and spend more. Thanks to accommodative lenders eager to provide

refinancings and home equity loans, Americans extracted $719 billion in cash

from their houses last year after a $633 billion withdrawal in 2004, according

to the Federal Reserve.

But the housing bubble is deflating rapidly. I expect at least a 20%

decline in median single-family house prices nationwide, and that number may be

way understated. A bursting of the bubble would force many homeowners to curb

their outlays in order to close the gaps between their income and spending

growth. That would surely precipitate a major recession that would become

global, given the dependence of most foreign countries on U.S. consumers to buy

the excess goods and services for which they have no other markets.

That is, unless another source of money can bridge the gap

between consumer incomes and outlays, just as house appreciation seamlessly

took over when stocks nosedived. What could that big new source of money be?

And would it be available soon, given the likelihood that house prices will

swoon in coming quarters?

One possible source of big, although not immediate, money to sustain

consumer spending is inheritance. Some estimates in the 1990s had the postwar

babies, who have saved little for their retirement, inheriting between $10

trillion and $41 trillion from their parents in the coming decades. But

subsequent work by AARP, using the Federal Reserve’s Survey of Consumer

Finances for 2004 and previous years, slashed the total for inheritances of all

people alive today to $12 trillion in 2005 dollars. Most of it, $9.2 trillion,

will go to pre-boomers born before 1946, only $2.1 trillion to the postwar

babies born between 1946 and 1964, and $0.7 trillion to the post-boomers.

Furthermore, the value of all previous inheritances as reported in the

2004 survey was $49,902 on average, with $70,317 for pre-boomers, $48,768 for

boomers and $24,348 for post-boomers. Clearly, these are not numbers that

provide for comfortable retirements and, therefore, allow people to continue to

spend like drunken sailors.

What other assets could consumers borrow against or liquidate to support

spending growth in the future? After all, they do have a lot of net worth,

almost $54 trillion for households and nonprofit organizations as of the end of

the first quarter. Nevertheless, there aren’t any other big assets left to tap.

Another big stock bonanza is unlikely for decades, and the real estate bubble

is deflating.

Deposits total $6.3 trillion, but the majority, $4.9 trillion worth, is

in time and savings deposits, largely held for retirement by financially

conservative people. Is it likely that a speculator who owns five houses has

sizable time deposits to fall back on? Households and nonprofits hold $3.2

trillion in bonds and other credit market instruments, but most owned by individuals

are in conservative hands. Life insurance reserves can be borrowed, but their

total size, $1.1 trillion, pales in comparison to the $1.8 trillion that

homeowners extracted from their houses in the 2003-2005 years. There’s $6.7

trillion of equity in noncorporate business, but the vast majority of that is

needed by typically cash-poor small businesses to keep their doors open.

Pension funds might be a source of cash for consumers who want to live it

up now and take the Scarlett O’Hara, “I’ll worry about that tomorrow” attitude

toward retirement. They totaled $11.1 trillion in the first quarter, but that

number includes public funds and private defined benefit plans that are seldom

available to pre-retirees unless they leave their jobs.

The private defined contribution plans, typically 401(k)s, totaled $2.5

trillion in 2004 and have been growing rapidly because employers favor them.

But sadly, many employees, especially those at lower income levels, don’t share

their bosses’ zeal. Only about 70% participate in their company 401(k) plans

and thereby take advantage of company contributions. Lower paid employees are

especially absent from participation, with 40% of those making less than

$20,000 contributing (60% of those earning $20,000 to $40,000), while 90% of

employees earning $100,000 or more participate.

Furthermore, the amount that employees could net from withdrawals from

defined contribution plans would be far less than the $2.5 trillion total,

probably less than the $1.8 trillion they pulled out of their houses from 2003

to 2005. That $2.5 trillion total includes company contributions that are not

yet vested and can’t be withdrawn. Also, withdrawals by those under 59½ years

old are subject to a 10% penalty, with income taxes due on the remainder.

With soaring stock portfolios now ancient history and leaping house prices about to be, no other sources, such as inheritance or pension fund withdrawals, are likely to fill the gap between robust consumer spending and weak income growth. Consumer retrenchment and the saving spree I’ve been expecting may finally be about to commence. And the effects on consumer behavior, especially on borrowing and discretionary spending, will be broad and deep.

Analysts' Forecasts and Brokerage-Firm Trading

THE ACCOUNTING REVIEW Vol. 79, No. 1 2004 pp. 125–149 Analysts’ Forecasts

and

Brokerage-Firm Trading Paul J. Irvine Emory University University of

Georgia

Collectively, these results suggest that analysts can generate higher trading

commissions through their positive stock recommendations than by biasing their

forecasts.

WHISPERS OF MERGERS SET OFF

BOUTS OF SUSPICIOUS TRADING...

August 27, 2006 NYTimes By GRETCHEN MORGENSONThe boom in corporate mergers is creating concern that

illicit trading ahead of deal announcements is becoming a systemic problem.

Sartre, Courtesy of

Etherzone.com, on the Typical Criminal american B**l S**t: "The official

rate of inflation is a lie. Look at the expense on essentials. The price tag of

food has gone through the roof. Energy, medical, insurance and education costs

are unbearable. As the rise in local and state taxes far out pace any minimal

reductions on the federal level. The huge balance of payments trade shortfall

is no accident. Government deficits grow, as massive debt piles up. No wonder

the laws of economic veracity require a loss of purchasing power in the value

of the currency".

YOU CAN'T BELIEVE A WORD THEY

SAY!