John

Hussman: Post Crash Bubbles

Excerpt from the Hussman Funds' Weekly Market Comment

(5/11/09):

It would be very convenient if it was

possible to buy the fear lows, participate in the bear market rallies, sell at

the peaks, and repeat. Unfortunately, “fear” lows are only evident in

hindsight, because as we saw in 2008, a deeply oversold market can become

spectacularly more oversold before recovering, and the “fast, furious” spikes

off of those lows are often followed by steep failures. Fear lows are only easy

to identify in hindsight.

Even if we have observed the ultimate

lows of this downturn (which I would not take as given), it does not follow

that the decline we've observed over the past 18 months will be progressively

recovered without a great deal of intervening difficulty. The S&P 500 has

retraced just over 25% of its bear market loss. The 904 level on the S&P

500 was a 25% retracement, and 977 would be a 1/3 retracement, which is not

unreasonable. Aside from such retracements, the idea of a “V-shaped” recovery

in the market is strongly odds with “post-crash” market behavior, which

generally features a long and drawn-out flat period for years afterward.

Given the enormous overhang of Alt-A and option-ARM resets scheduled to begin

later this year, extending into 2012, such a profile would not be surprising in

the present case.

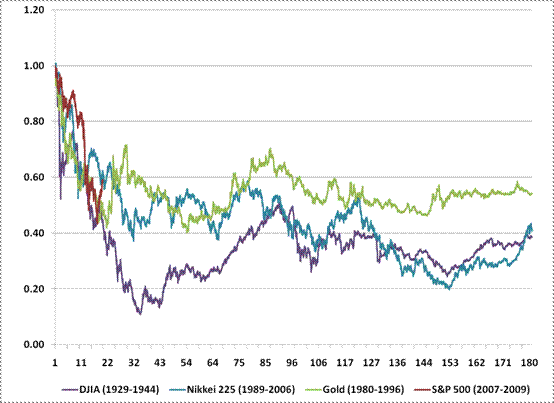

To put the current downturn into similar

context, the chart below overlays several historical crashes, with the time

scale measured in months. The downturns include the Great Depression (purple),

the Japanese Nikkei index which peaked in 1989 (blue), the gold market which

peaked in 1980 (green), and the S&P 500 which peaked in 2007 (red). Thanks

to Bill Hester for preparing this overlay.

Note that during all of these downturns,

the markets did experience very powerful intervening advances as well (indeed,

the rally off of the initial 1929 market crash approached 50% before failing).

In each case, however, the fundamentals of the preceding bubble had been

broken and it took years for the markets and economy to adjust. In the

case of gold, the shift in fundamentals was the end of double-digit inflation.

In the other instances, including the present one, the shift was from a steeply

leveraged economy to a deleveraging one.

To a great extent, the optimism of

investors is based primarily on economic “flow” data (spending, job losses,

confidence measures) that remain poor, but have been “less bad” than expected.

What concerns me far more, however, is that there is a second and almost

equivalent mountain of mortgage resets and probable defaults that will begin

later this year and extend into 2012. While our unelected bureaucrats have

spent over a trillion dollars to make reckless lenders whole, they have done

nothing to materially ease foreclosures or avert the oncoming second wave.