Sliding Back Into the Great

Recession

Steven Hansen 1-24-10 [this is a rather mild if not optimistic

assessment inasmuch as it relies upon and inappropriately lends greater

credence to Leading Economic Indicators index which is skewed to the upside

owing to the overvalued bubble stock market component thereof and he himself

has some long positions which are contraindicated by reality – but charts and

data are always helpful as here provided]

This is the week of the

perfect storm. Investors do not like uncertainty, and prefer living with known

conditions – good or bad. This week the political landscape exploded with the

loss of the Democrats super-majority in the Senate throwing the health care

legislation (and current health care investment bets) into limbo.

In an obvious political

move to regain momentum, our President went on a populist rampage against the

financial industry which sent the markets in a downward spiral.

Concurrently from the

economic side, I was stunned by the very negative data from the Philly Fed who

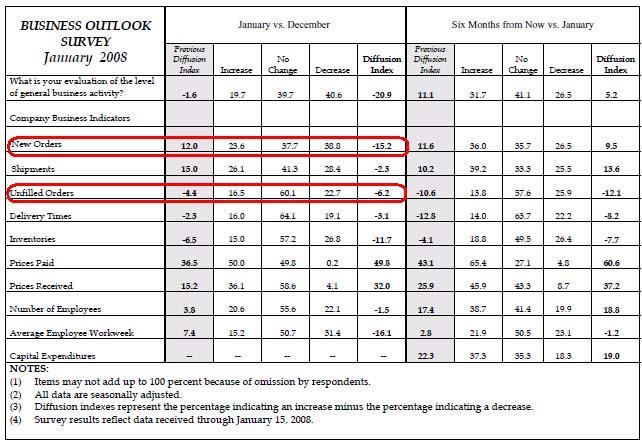

released their survey of manufacturers for Jan 2010 (pdf):

Activity in the region’s manufacturing sector weakened this

month, according to firms surveyed for the January Business Outlook Survey.

The general activity and new orders indexes fell sharply this month, and

indexes for shipments and employment also turned negative. A significant share

of firms reported a rise in prices for inputs and for their own manufactured

goods. Also this month, the region’s manufacturing executives were less

optimistic about future activity, and most future indicators have fallen

considerably over the past three months.

New orders and unfilled orders are negative MoM – extremely

negative. WTF?

This is a subjective survey a month ahead of real quantitative

data. This survey is diametrically opposite to the results of the NY Fed

manufacturing survey which I analyzed last week. If this survey is proven by

hard data, this will be the first indication we are sliding back into a

recession.

It also begs the question – did we ever leave the Great

Recession?

“The recession is over (if you happen to work at Goldman

Sachs).” [Hat tip to Mish]

Or why do the leading economic indicators continue to show

growth?

The leading indicators are likely correct. These indicators are

geared more towards forecasting GDP – and not Joe Sixpack’s world. Some

analysts expect a very strong 4Q2009 GDP. The first release of 4Q2009 GDP will

be at the end of this month.

Sometime in the past, GDP and Joe Sixpack’s world went

their separate ways. We began to lose the linkage between jobs and GDP in 1990.

To illustrate this point using chained 2005 dollars, we entered

2000 with a GDP of $11 trillion. Most likely, we will have left 2009 with a GDP

of $13 trillion. Over this 10 year period GDP expanded 18% in inflation

adjusted terms - yet over the same period we did not increase the size of the

workforce.

The only conclusion I can draw from this is that GDP

expansion must be higher than 1.5% to 2% to create jobs.

Yet, in 3Q2009, with a GDP increase of 2.2% - we still were

unable to increase the number of jobs in America. It may be that the disconnect

between jobs and GDP is growing, and we may well need over 3% GDP growth to

generate jobs.

My belief remains that GDP no longer is the primary tool for

measuring the American economy. GDP is a relic from the days of the industrial

revolution.

The people who date our recessions - NBER’s Business Cycle

Dating Committee – released the following statement supposedly on November 24, 2009 (hat

tip to The Big Picture who found this statement this

week):

The NBER’s Business Cycle Dating Committee maintains a

chronology of the U.S. business cycle. The chronology comprises alternating

dates of peaks and troughs in economic activity. A recession is a period

between a peak and a trough, and an expansion is a period between a trough and

a peak. During a recession, a significant decline in economic activity spreads

across the economy and can last from a few months to more than a year.

Similarly, during an expansion, economic activity rises substantially, spreads

across the economy, and usually lasts for several years.

In both recessions and expansions, brief reversals in economic

activity may occur—a recession may include a short period of expansion followed

by further decline; an expansion may include a short period of contraction

followed by further growth. The Committee applies its judgment based on the

above definitions of recessions and expansions and has no fixed rule to

determine whether a contraction is only a short interruption of an expansion,

or an expansion is only a short interruption of a contraction. The most recent

example of such a judgment that was less than obvious was in 1980-1982, when

the Committee determined that the contraction that began in 1981 was not a

continuation of the one that began in 1980, but rather a separate full

recession.

The Committee does not have a fixed definition of economic

activity. It examines and compares the behavior of various measures of broad

activity: real GDP measured on the product and income sides, economy-wide

employment, and real income. The Committee also may consider indicators that do

not cover the entire economy, such as real sales and the Federal Reserve’s

index of industrial production (IP).

The Committee’s use of these indicators in conjunction with the broad measures

recognizes the issue of double-counting of sectors included in both those

indicators and the broad measures. Still, a well-defined peak or trough in real

sales or IP might help to determine the overall peak or trough dates, particularly

if the economy-wide indicators are in conflict or do not have well-defined

peaks or troughs.

This was under the radar as it appears neither I nor others

received notification – and was not picked up by any media source. Now compare

the above NBER statement supposedly released on November 24th to the official

NBER Recession Dating Procedure which says in part:

In choosing the dates of business-cycle turning points, the

committee follows standard procedures to assure continuity in the chronology.

Because a recession influences the economy broadly and is not confined to one

sector, the committee emphasizes economy-wide measures of economic activity. The

committee views real GDP as the single best measure of aggregate economic

activity. In determining whether a recession has occurred and in identifying

the approximate dates of the peak and the trough, the committee therefore

places considerable weight on the estimates of real GDP issued by the Bureau of

Economic Analysis of the U.S. Department of Commerce. The traditional role of

the committee is to maintain a monthly chronology, however, and the BEA's real

GDP estimates are only available quarterly. For this reason, the committee refers

to a variety of monthly indicators to determine the months of peaks and

troughs.

It seems the NBER with their recent statement that GDP may not

be the primary measurement of the economy anymore. This is in direct conflict

with their procedures, but a welcome bit of fresh air.

It boils down to whether it is best to believe we are in a

recession, and keep the political emphasis on taking actions to make the

economy better – or simply ignore poor economic conditions telling the masses

the economy is improving.

Either way, I have no hope the President, Congress or the Fed

have any clue how to get this beast moving except through letting time cure the

economic ills or spouting populist agenda issues.

There continues to be no evidence the economy is expanding other

than the economic bounce you get when inventories deplete. The jobs situation

is worse than any four letter word I can use.

Now the Philly Fed survey has provided a whiff of further

contraction.

Hopefully, this survey is an anomaly.

Other Economic News this Week

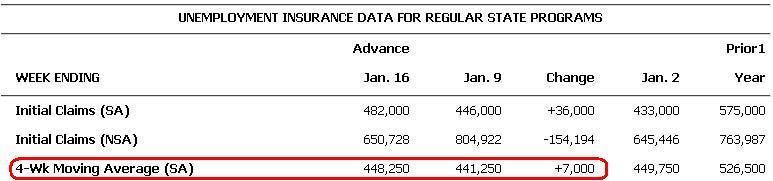

Initial unemployment claims for the week ending January 16, 2010 increased slightly and is

hovering just below the level where historically payroll employment begins to

grow. I have heard many explanations for the increase this week, and this is

why I continue to monitor unemployment claims using a 4 week average.

The initial claims picture, no matter how you spin it, is headed

downward at a painfully slow rate. The real question is whether America is

creating jobs as historical data might suggest.

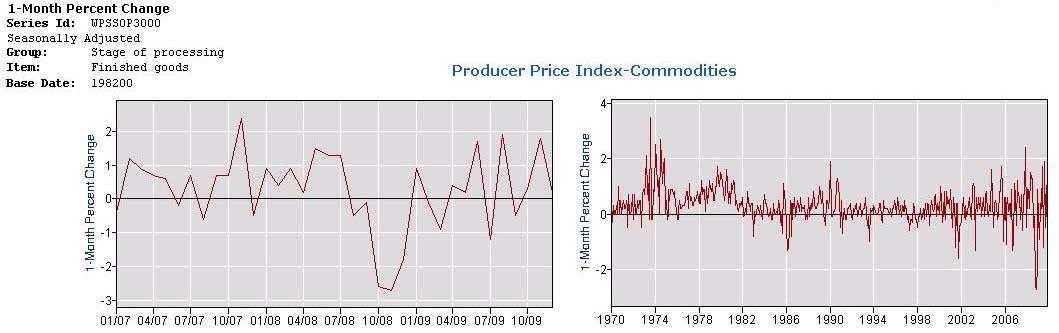

The government’s statement on the December

2009 (pdf) Producer Price Index:

The Producer Price Index for Finished Goods moved up 0.2% in

December, seasonally adjusted. This rise followed a 1.8% advance in November

and a 0.3% increase in October. At the earlier stages of processing, prices

received by producers of intermediate goods rose 0.5% and the crude goods index

moved up 1.0 percent. On an unadjusted basis, prices for finished goods

advanced 4.4 percent in 2009, after falling 0.9% in 2008.

This month, if you exclude food and energy – what the economists

love to call core index items – the finished goods were unchanged MoM. However,

the intermediate goods and crude goods were up – but within the range of the

last 12 months.

Overall, there was nothing noteworthy in this release. I have,

however, included two graphs over the movement of the finished goods PPI since

2007 and 1970.

What is interesting is the ever increasing volatility of this

pricing index. It is beginning to look like a seismograph during a San Andreas

event. Are there any seismologist’s out there?

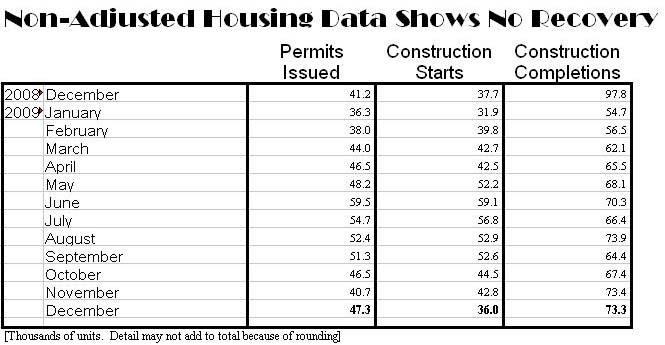

The government’s words on residential new construction data for December 2009:

Privately-owned housing units authorized by building permits in

December were at a seasonally adjusted annual rate of 653,000. This is 10.9%

above the revised November rate of 589,000 and is 15.8% above the December 2008

estimate of 564,000.

Privately-owned housing starts in December were at a seasonally

adjusted annual rate of 557,000. This is 4.0% below the revised November

estimate of 580,000, but is 0.2% above the December 2008 rate of 556,000.

Privately-owned housing completions in December were at a

seasonally adjusted annual rate of 768,000. This is 11.2% below the revised

November estimate of 865,000 and is 25.3% below the December 2008 rate of

1,028,000.

There is no evidence that any recovery is underway in this

sector using unadjusted data. Permits are up MoM and YoY (but remains range

bound), Starts and completions are down MoM and YoY. Historically, new home

starts pick up during recoveries. This recovery is different as we have a

surplus of houses. Therefore our “recovery” without residential construction

spending will be weaker than past recoveries.

The weekly Mortgage Bankers Association new mortgage application

data for the week ending 15 Jan 2010 improved slightly but remains

about half of the level of earlier this year using seasonally adjusted data.

The 30 year fixed mortgage rate dropped 13 basis points to 5.00%.

Bankruptcies this week: Morris Publishing Group, Atrium

Companies

Economic Forecasts Published this Past Week

The

Economic Cycle

Research Institute (ECRI) released their Weekly Leading Index which

its yearly growth rate slipped slightly – but the WLI is still setting new

highs. Lakshman Achuthan, Managing Director at ECRI added:

The

Economic Cycle

Research Institute (ECRI) released their Weekly Leading Index which

its yearly growth rate slipped slightly – but the WLI is still setting new

highs. Lakshman Achuthan, Managing Director at ECRI added:

The index's annualized growth rate slipped again to a 19-week

low of 23.4% from 23.7% the previous week, which was revised up from an

original 23.5%. It marked the lowest yearly growth reading since the gauge

reached a record high in October. Still, with WLI levels continuing to rise,

the recovery will continue to gain ground in the months ahead. The yearly

growth rate figure sometimes moves inversely to the index level because the

latter is derived from a four-week moving average

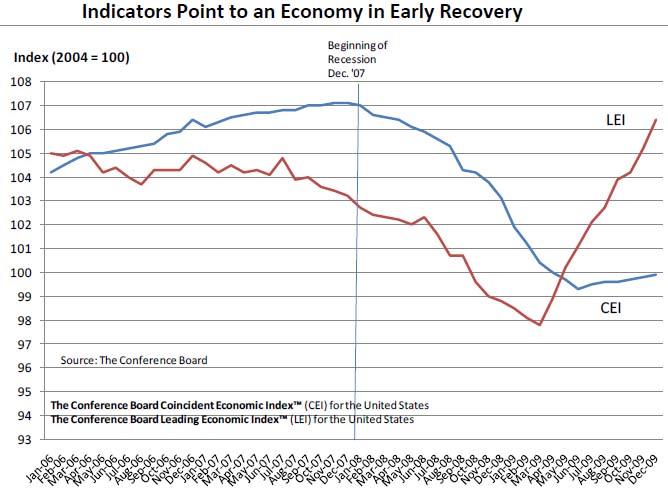

The Conference Board issued their Leading and Coincident

Economic Indexes for December 2009 (pdf). Statements from their

official news release:

The Conference Board LEI for the U.S. increased sharply in

December, and has risen steadily for nine consecutive months. The six-month

growth rate has picked up slightly to 5.2 percent (about a 10.8 percent annual

rate) in the period through December, substantially higher than earlier in the

year. In addition, the strengths among the leading indicators have remained

very widespread in recent months.

The indicators point to an economy in early recovery. The

coincident economic index shows slow expansion of economic activity through

December. The leading economic index suggests that the pace of improvement

could pick up this spring.

The Conference Board Coincident Economic Index™ (CEI)

for the U.S. rose 0.1 percent in December, following a 0.1% increase in both

November and October. The Conference Board Lagging Economic Index™ (LAG)

declined 0.2% in December, following a 0.5% decline in November, and a 0.2%

decline in October.

Disclosure: Author holds positions in GLD,

XPH,

XLB,

XLV,

FTR,

IOO,

HYG,

KSWS,

PIN,

WMT,

GDX,

Physical Gold - as well as numerous puts and calls which comprise less than 3%

of my portfolio